|

Franklin India Corporate Debt Fund

As on April 30, 2026 |

|

|

An open ended debt scheme predominantly investing in AA+ and above rated corporate bonds

SCHEME CATEGORY

Corporate Bond Fund

SCHEME CHARACTERISTICS

Min 80% in Corporate Bonds (only AA+ and above)

INVESTMENT OBJECTIVE

The investment objective of the Scheme is primarily to provide investors Regular income and Capital appreciation.

DATE OF ALLOTMENT:

June 23, 1997

FUND MANAGER(S):

Anuj Tagra (w.e.f. March 07, 2024)

Chandni Gupta (w.e.f. March 07, 2024)

Rahul Goswami (w.e.f. October 6, 2023)

BENCHMARK:

NIFTY Corporate Bond Index A-II

(w.e.f. April 1, 2024)

| MATURITY & YIELD | |

| RESIDUAL MATURITY/AVERAGE MATURITY | 3.81 years |

| ANNUALISED PORTFOLIO YTM# | 7.51% |

| MODIFIED DURATION | 1.84 years |

| MACAULAY DURATION | 1.97 years |

BASE EXPENSE RATIO#: 0.63% BASE EXPENSE RATIO# (DIRECT) : 0.21%

#Base Expense Ratio (BER) is the actual expense ratio charged as per the AUM slabs and within the BER limits prescribed in Regulation 66 of SEBI MF regulations. BER excludes brokerage and transaction costs incurred towards execution of trades and the applicable statutory levies as on that date. Brokerage and transaction costs incurred towards execution of trades and statutory levies are charged, at actuals, and is over and above the BER.

For Total Expense Ratio (TER) and break up of TER i.e., BER, brokerage and transaction costs and statutory levies, please refer to daily TER disclosures on our website www.franklintempletonindia.com. For detailed understanding of TER, please refer to the TER note on our website. MINIMUM INVESTMENT/

MULTIPLES FOR NEW INVESTORS:

Plan A :Rs 10,000/1 MINIMUM INVESTMENT FOR SIP

Rs 500/1

ADDITIONAL INVESTMENT/

MULTIPLES FOR EXISTING INVESTORS Plan A : Rs1000/1 LOAD STRUCTURE:

| Plan A : Entry Load | : | Nil |

| Exit Load (for each purchase of Units) | : | Nil Sales suspended in Plan B - All Options |

| Different plans have a different expense structure

| ||

| Growth Plan | Rs 104.2961 |

| Annual IDCW Plan | Rs 16.6463 |

| Monthly IDCW Plan | Rs 15.1608 |

| Quarterly IDCW Plan | Rs 12.0002 |

| Half-yearly IDCW Plan | Rs 12.4123 |

| Direct - Growth Plan | Rs 113.4404 |

| Direct - Annual IDCW Plan | Rs 18.6690 |

| Direct - Monthly IDCW Plan | Rs 16.9485 |

| Direct - Quarterly IDCW Plan | Rs 13.6255 |

| Direct - Half-yearly IDCW Plan | Rs 14.6370 |

| As per the addendum dated March 31, 2021, the Dividend Plan has been renamed to Income Distribution cum capital withdrawal (IDCW) Plan with effect from April 1, 2021 | |

| FUND SIZE (AUM) | |

| Month End | Rs1283.40 Crores |

| Monthly Average | Rs1274.11 Crores |

| Company Name | Company Ratings | Market Value (including accrued interest, if any) (Rs. in Lakhs) | % of assets | |||

| Poonawalla Fincorp Ltd* | CRISIL AAA | 10,555.10 | 8.22 | |||

| LIC Housing Finance Ltd* | CARE AAA | 5,865.83 | 4.57 | |||

| RJ Corp Ltd* | CRISIL AAA | 5,509.55 | 4.29 | |||

| Summit Digitel Infrastructure Ltd* | CRISIL AAA | 5,048.62 | 3.93 | |||

| Embassy Office Parks Reit* | CRISIL AAA | 4,986.57 | 3.89 | |||

| Jubilant Beverages Ltd* | CRISIL AA | 4,621.74 | 3.60 | |||

| Jubilant Bevco Ltd | CRISIL AA | 4,437.77 | 3.46 | |||

| Bharti Telecom Ltd | CRISIL AAA | 4,297.75 | 3.35 | |||

| Kotak Mahindra Investments Ltd | CRISIL AAA | 3,673.84 | 2.86 | |||

| LIC Housing Finance Ltd | CRISIL AAA | 3,062.60 | 2.39 | |||

| HDB Financial Services Ltd | CRISIL AAA | 2,716.58 | 2.12 | |||

| Tata Communications Ltd | CARE AAA | 2,632.56 | 2.05 | |||

| Bajaj Finance Ltd | IND AAA | 2,542.52 | 1.98 | |||

| HDFC Bank Ltd | ICRA AAA | 1,075.38 | 0.84 | |||

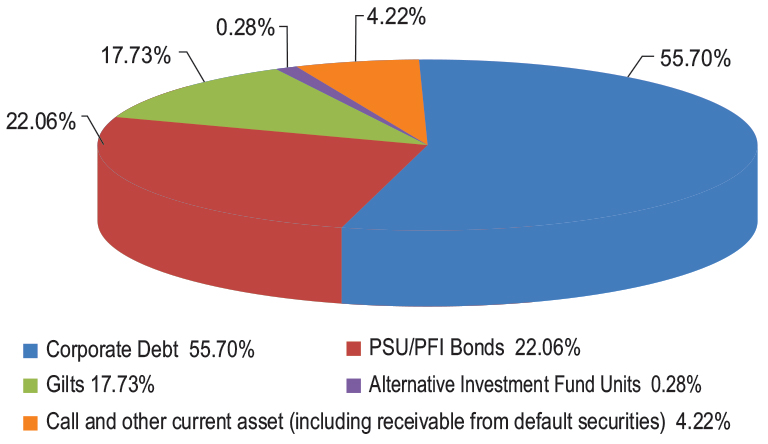

| Total Corporate Debt | 61,026.41 | 47.55 | ||||

| Power Finance Corporation Ltd* | ICRA AAA | 8,004.97 | 6.24 | |||

| National Bank For Agriculture & Rural Development* | IND AAA | 7,594.39 | 5.92 | |||

| REC Ltd* | CRISIL AAA | 5,342.32 | 4.16 | |||

| Power Finance Corporation Ltd | CRISIL AAA | 4,513.51 | 3.52 | |||

| Housing & Urban Development Corporation Ltd | ICRA AAA | 2,631.94 | 2.05 | |||

| Small Industries Development Bank Of India | CRISIL AAA | 2,624.31 | 2.04 | |||

| National Housing Bank | CARE AAA | 2,512.56 | 1.96 | |||

| REC Ltd | CARE AAA | 2,492.42 | 1.94 | |||

| National Bank For Agriculture & Rural Development | ICRA AAA | 2,476.00 | 1.93 | |||

| Small Industries Development Bank Of India | CARE AAA | 2,097.87 | 1.63 | |||

| REC Ltd | ICRA AAA | 1,571.21 | 1.22 | |||

| Total PSU/PFI Bonds | 41,861.49 | 32.62 | ||||

| 7.66% Maharashtra SDL (04-Mar-2047)* | SOVEREIGN | 5,477.17 | 4.27 | |||

| 7.62% Punjab SDL (28-Jan-2033) | SOVEREIGN | 2,535.21 | 1.98 | |||

| 6.90% GOI 2065 (15-APR-2065) | SOVEREIGN | 2,323.64 | 1.81 | |||

| 7.73% Andhra Pradesh SDL (23-Mar-2032) | SOVEREIGN | 1,526.69 | 1.19 | |||

| 6.48% Andhra Pradesh SDL (15-Jul-2032) | SOVEREIGN | 967.29 | 0.75 | |||

| 7.65% Bihar SDL (24-Dec-2033) | SOVEREIGN | 960.77 | 0.75 | |||

| 7.15% Andhra Pradesh SDL (04-Mar-2031) | SOVEREIGN | 500.65 | 0.39 | |||

| 7.17% Rajasthan SDL (02-Mar-2032) | SOVEREIGN | 497.04 | 0.39 | |||

| 7.64% Uttarakhand SDL (24-Dec-2032) | SOVEREIGN | 108.97 | 0.08 | |||

| 7.32% Chhattisgarh SDL (05-Mar-2037) | SOVEREIGN | 51.24 | 0.04 | |||

| 7.32% West Bengal SDL (05-Mar-2038) | SOVEREIGN | 48.58 | 0.04 | |||

| Total Gilts | 14,997.24 | 11.69 | ||||

| Total Debt Holdings | 1,17,885.13 | 91.85 | ||||

| Company Name | No.of Shares | Market Value(Rs. in Lakhs) | % of Assets | |||

| Alternative Investment Fund Units | ||||||

| Corporate Debt Market Development Fund Class A2 | 3,174 | 372.94 | 0.29 | |||

| Total Alternative Investment Fund Units | 372.94 | 0.29 | ||||

| Total Holdings | 1,18,258.07 | 92.14 | ||||

| Margin on Derivatives | 0.00 | 0.00 | ||||

| Call,cash and other current asset | 10,082.37 | 7.86 | ||||

| Total Asset | 1,28,340.44 | 100.00 | ||||

| * Top 10 holdings | ||||||

Outstanding Interest Rate Swap Position

| Contract Name | Notional Value (In Lakhs) | % of assets |

| STANDARD CHARTERED BANK (Pay Fixed - Receive Floating) | 6,500 | 5.06 |

| DBS BANK LTD (Pay Fixed - Receive Floating) | 5,000 | 3.90 |

| ICICI SECURITIES PRIMARY DEALERSHIP LTD (Pay Fixed - Receive Floating) | 2,500 | 1.95 |

| ICICI SECURITIES PRIMARY DEALERSHIP LTD (Pay Fixed - Receive Floating) | 2,500 | 1.95 |

| IDFC FIRST BANK LTD (Pay Fixed - Receive Floating) | 2,500 | 1.95 |

| STANDARD CHARTERED (Pay Fixed - Receive Floating) | 2,500 | 1.95 |

| STANDARD CHARTERED (Pay Fixed - Receive Floating) | 2,500 | 1.95 |

| Total Interest Rate Swap | 24,000 | 18.70 |

@ TREPs /Reverse Repo : 5.48%, Others (Cash/ Subscription receivable/ Redemption payable/ Receivables on sale/Payable on Purchase/ Other Receivable / Other Payable) : 2.38%

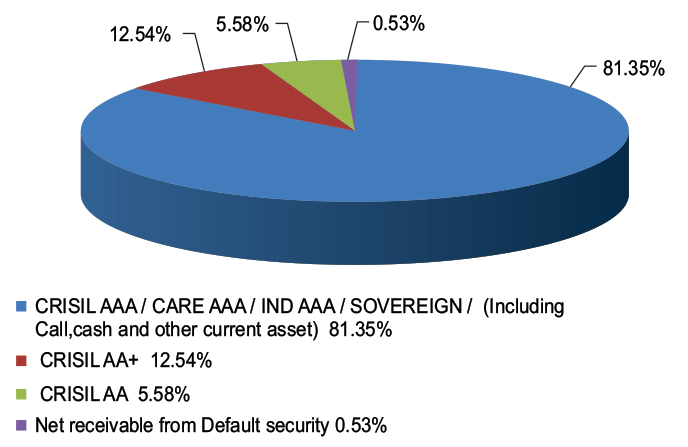

All investments in debt funds are subject to various types of risks including credit risk, interest rate risk, liquidity risk etc. Some fixed income schemes may have a higher

concentration to securities rated below AA and therefore may be exposed to relatively higher risk of downgrade or default and the associated volatility in prices which could

impact NAV of the scheme. Credit rating issued by SEBI registered entities is an opinion of the rating agency and should not be considered as an assurance of repayment by

issuer. There is no assurance or guarantee of principal or returns in any of the mutual fund scheme.

This scheme has exposure to floating rate instruments . The duration of these instruments is linked to the interest rate reset period. The interest rate risk in a floating rate

instrument or in a fixed rate instrument hedged with derivatives is likely to be lesser than that in an equivalent maturity fixed rate instrument. Under some market

circumstances the volatility may be of an order greater than what may ordinarily be expected considering only its duration. Hence investors are recommended to consider the

unadjusted portfolio maturity of the scheme as well and exercise adequate due diligence when deciding to make their investments.